Navigating Sourcing, Quality Shifts and Geopolitical Headwinds

6 MIN READ

By Franziska Finck — March 25, 2026

Our Monthly Olive Oil Market Report blends real-time data with field insights to

support your private label retail strategy.

Want it monthly?

Sign up hereWhat’s Happening This Month?

The Spanish market remains stable with balanced supply and steady demand. Trading is cautious as buyers and sellers cover only short-term needs rather than building large stocks. This stability is supported by the final Mediterranean harvest projections.

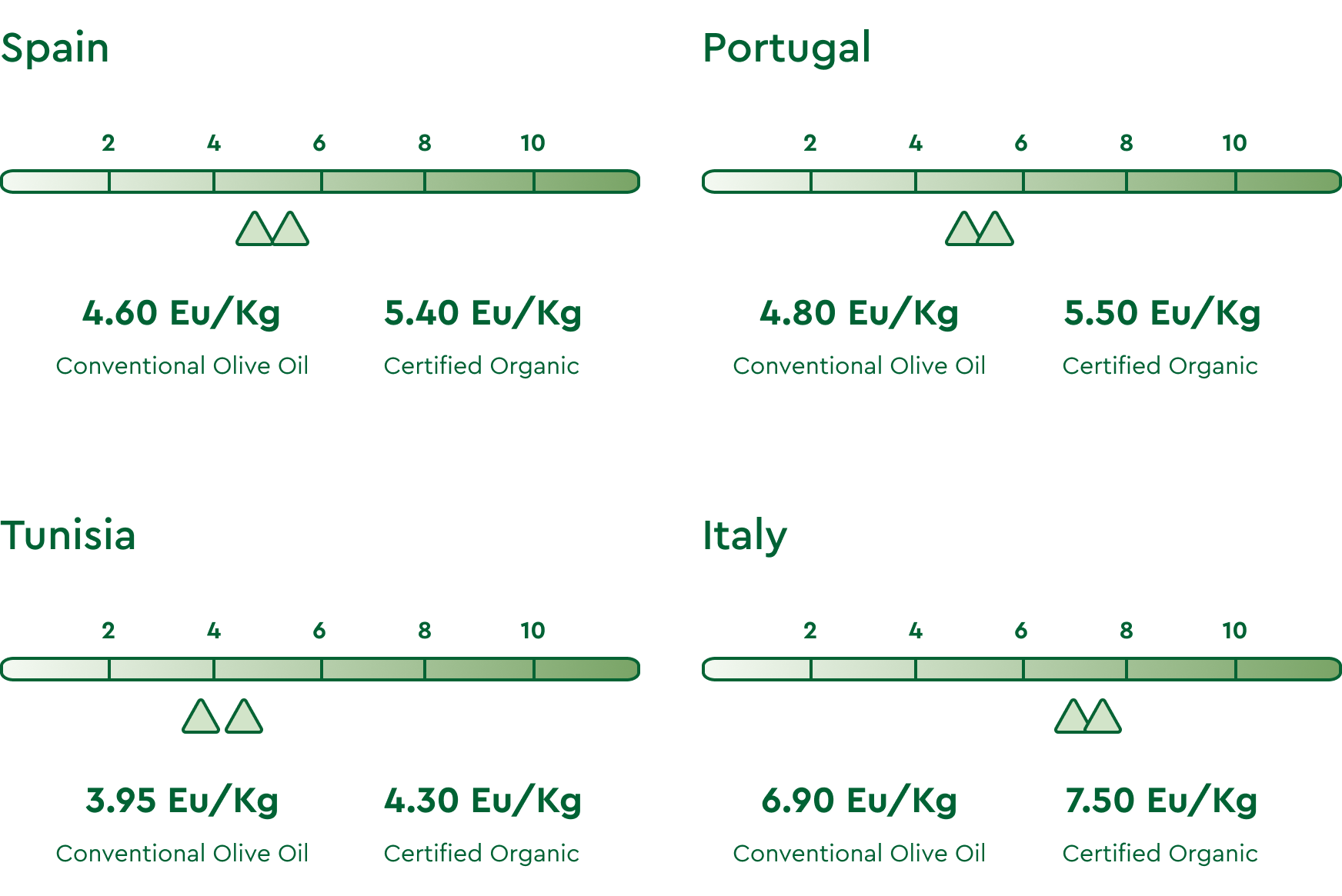

Export prices for pesticide-free EVOO vary significantly by origin.

Spain averages 4.60 Eu/Kg for conventional and 5.40 Eu/Kg for organic, while Portugal is slightly higher at 4.80 Eu/Kg and 5.50 Eu/Kg. Tunisia offers the lowest prices at 3.95 Eu/Kg (conventional) and 4.30 Eu/Kg (organic). Italy remains the highest at 6.90 Eu/Kg for conventional and 7.50 Eu/Kg for organic.

Compared to our last market report, price levels have remained largely unchanged. These regional price disparities reflect the different production outlooks, with Tunisia’s high-volume projections acting as a weight on Mediterranean bulk pricing.

In the higher quality segment, a growing scarcity of premium-grade oils is contributing to firmer values.

This trend reflects a widening gap between the high-volume bulk olive oil market and the limited availability of extra virgin olives meeting strict retail and chemical standards. Retail B2B procurement teams are currently concentrating on locking in quality-certified volumes for their programs, securing supply before the second half of 2026, to ensure sufficient stock to carry them through to the start of the new year.

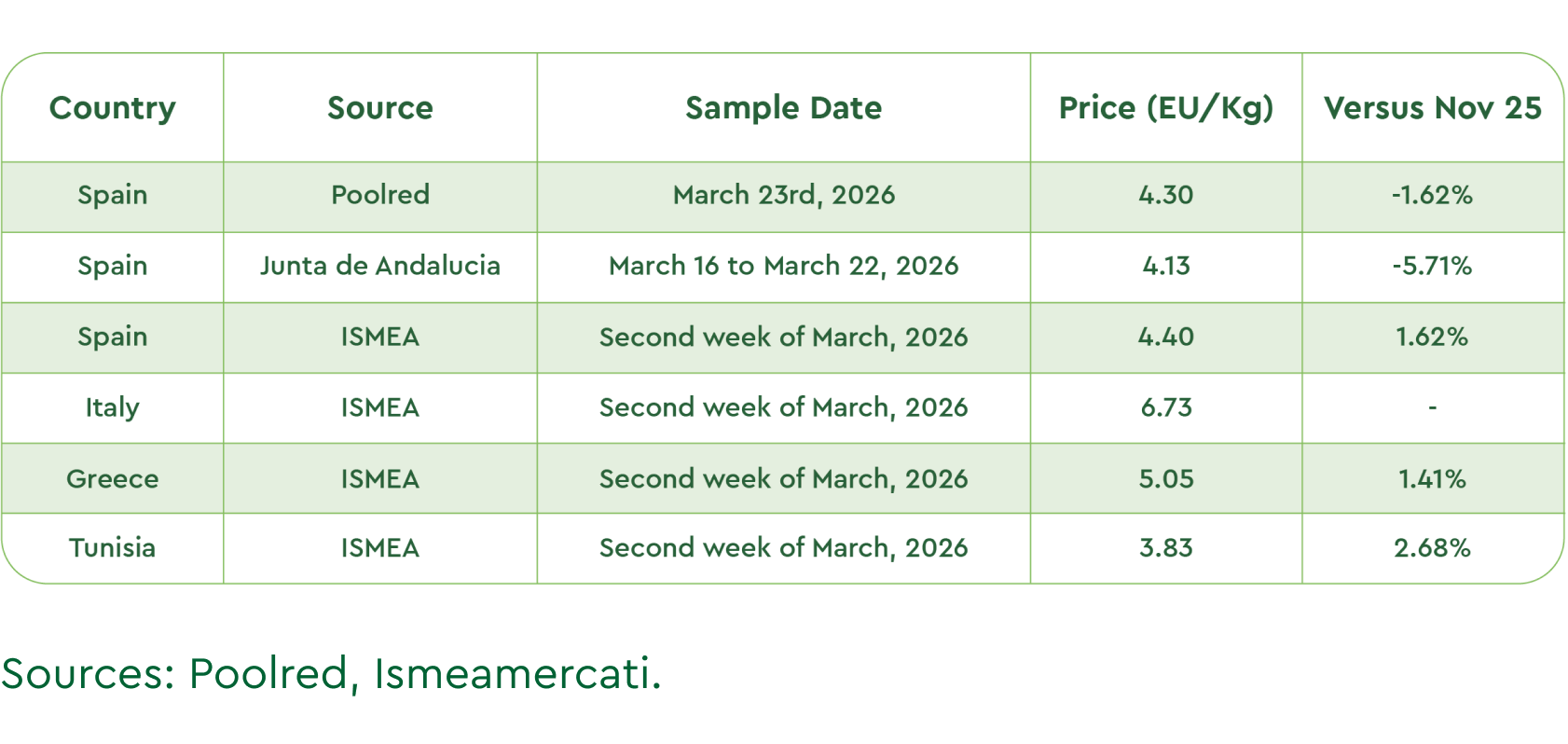

The main platforms that track average price developments across individual countries, show the following picture:

Latest Olive Oil Market Figures from Official Industry Sources

**Note: Reported prices are averages across multiple quality grades. Premium, traceable, clean, pesticide-free extra virgin olive oil typically trades at higher values.

**Note: Reported prices are averages across multiple quality grades. Premium, traceable, clean, pesticide-free extra virgin olive oil typically trades at higher values.

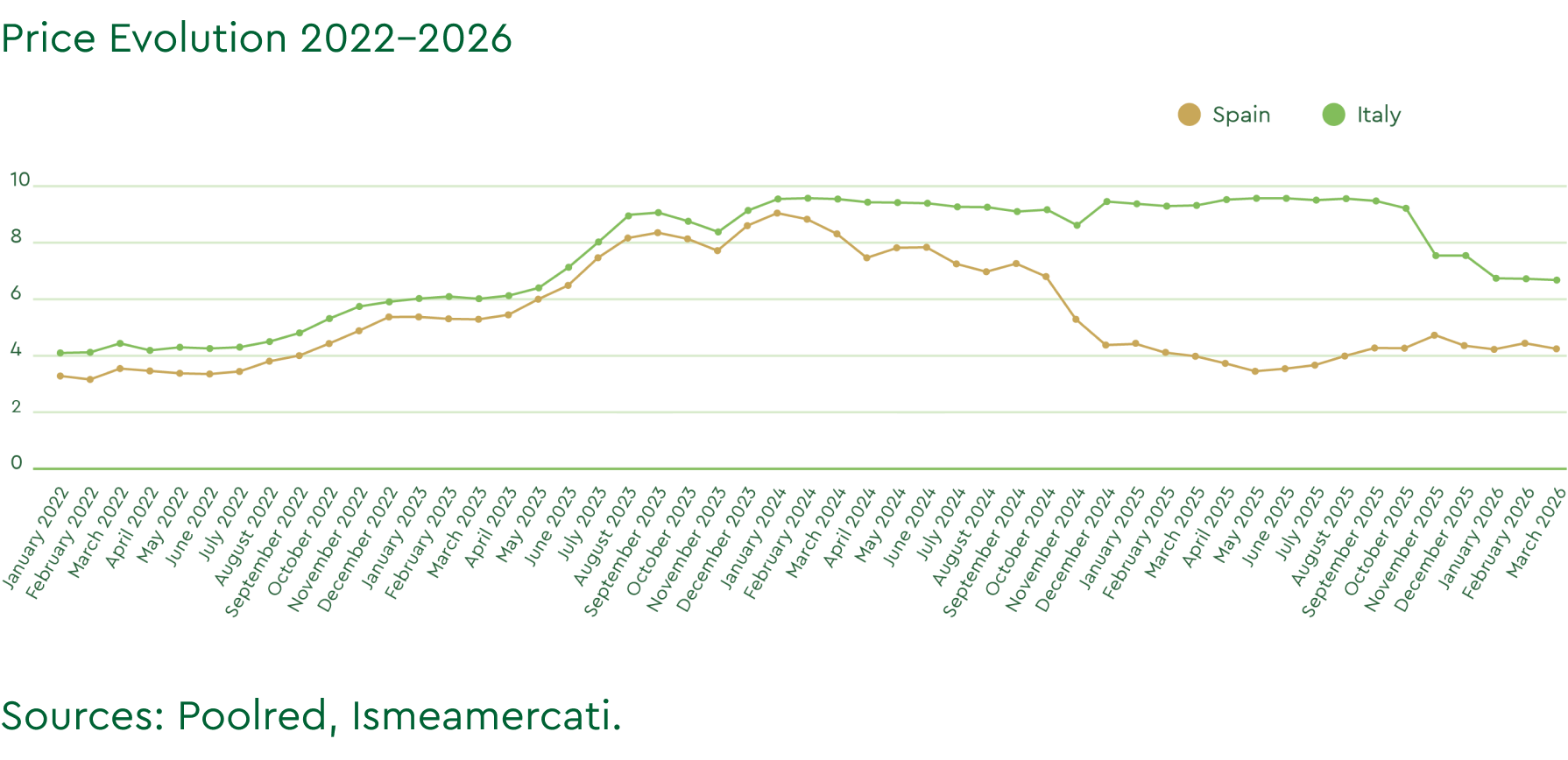

Extra Virgin Olive Oil Price Evolution

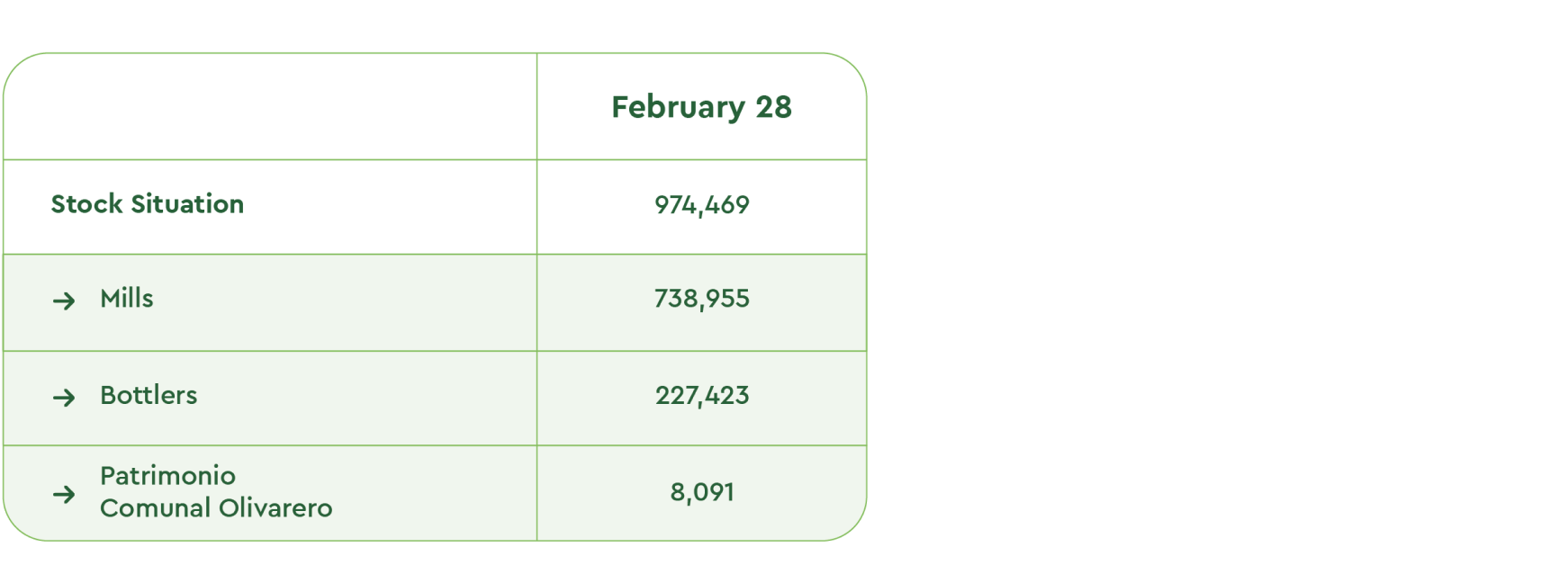

Spain: Production, Demand & Stocks by End of February

As of February 2026, cumulative Spanish production reached 1,193,767 tons, with 141,135 tons milled during the month. While the peak harvest has concluded, total output remains 15% below February 2025 levels and significantly trails the IOC’s 1.372 million tonne seasonal forecast. Market demand remains robust, with February off-take reaching 115,042 tons.

Total campaign sales now exceed 619,000 tons, representing over 50% of year-to-date production. ASAJA Jaén confirms that the marketing pace is 30,000 tons ahead of last season, a critical factor for price stability and the prevention of excessive carryover stocks.

The outlook for the 2026/27 Spanish harvest cycle is generally optimistic, with early 2026 rainfall leading to a consensus among industry participants about a potential output of 1.7 million. This optimism provides a long-term buffer, even as the current 2025/26 market remains in a period of technical adjustment.

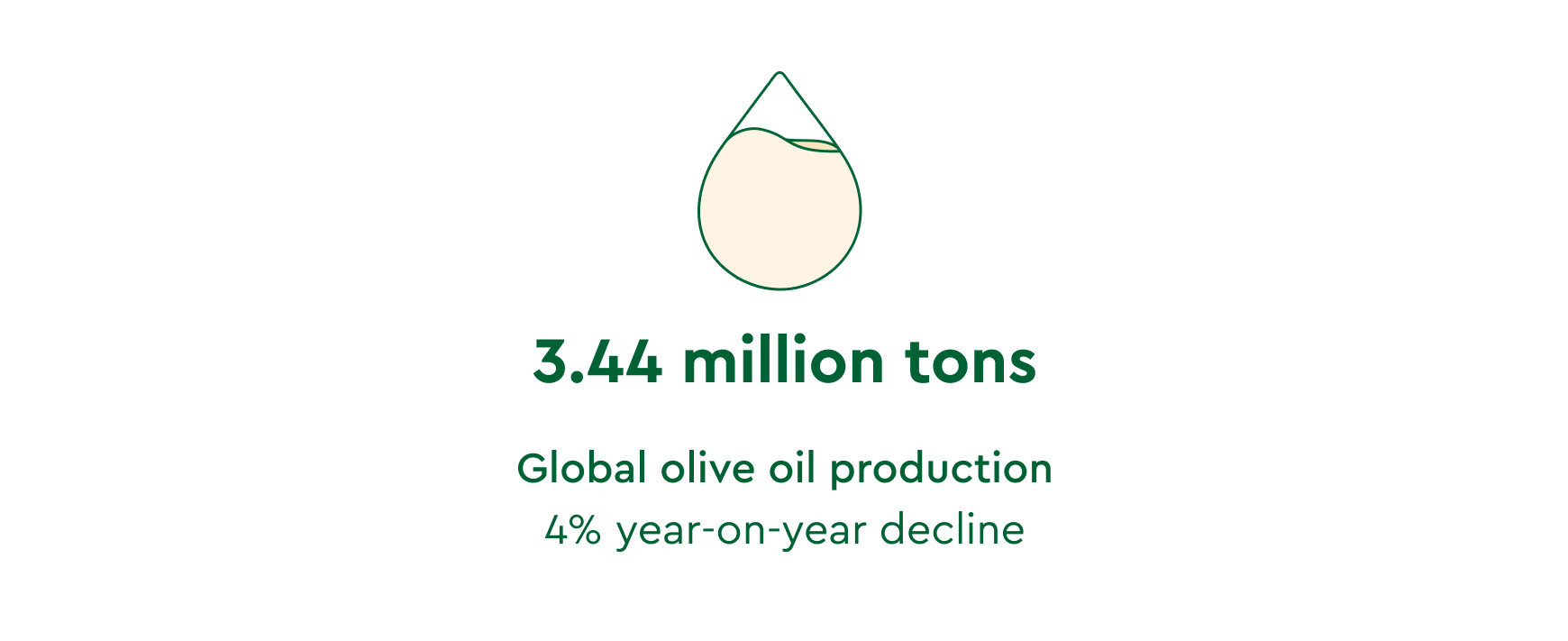

Global Olive Oil Market 2025/26: Solid Supply Amid Slight Production Decline

The Spanish trade magazine Mercacei reports a normalized 2025/26 global olive oil campaign following previous record peaks. Global production is estimated at 3.44 million tons, representing a 4% year-on-year decline while remaining at a historically high level.

EU output is projected at 2.06 million tons. Spain leads with 1.37 million tons despite a marginal decline, while Italy recovered to 300,000 tons. Conversely, Greece and Portugal face weather-driven reductions. Non-EU production totals 1.21 million tons, where Tunisia reached 450,000 tons and Morocco shows rapid expansion. Turkey dropped to 290,000 tons, reflecting a typical biennial bearing cycle.

On the demand side, global consumption remains stable at 3.25 million tons, supported by growth in non-traditional markets. International trade continues to expand, with imports exceeding 1.2 million tons. The 2025/26 campaign underscores structural climate sensitivity and the rising influence of non-EU origins within a resilient global market.

US Market focus: tariffs, consumption and import spike

According to the International Olive Oil Council, all-grades olive oil imports into the U.S. declined 1.6% during Q1 of the 2025/26 crop year. This contraction is most likely a correction following the June 2025 import spike, when volumes reached 66,000 MT (+99% YoY) due to importer front-loading ahead of anticipated new import taxes.

According to U.S. import data, a strong volume driver is now the Virgin olive oil grade, with free acidity ≤2.0% (HS 1509.30). Spanish growth in this segment was supported by high domestic stock levels and competitive pricing against Turkey and Tunisia, the other two lead players in the sector, followed by Italy.

Effective February 24, 2026, the U.S. implemented a 10% temporary surcharge under Section 122, replacing previous origin-specific taxes on the EU and Tunisia. This shift follows U.S. court rulings that limited the application of broader executive-led tariffs. The 10% rate is valid for 150 days and provides a relative cost advantage compared to the previously expected 15%. Markets are currently integrating these new costs into landed pricing for the Q2 shipping cycle.

Despite trade volatility, the USDA forecasts record U.S. consumption of 478,000 MT for 2025/26. Structural demand remains strong, with U.S. household penetration now at ~48% (Nielsen, 2025), up from ~30% in 2021. With over 97% of supply being imported, the U.S. market growth remains highly dependent on Mediterranean crop yields and evolving trade policy.

Final Thoughts for 2026 Strategic Procurement

Late rains in Spain and Morocco reduced EVOO availability, favoring Virgin (HS 1509.30) and Lampante grades. High-quality EVOO sourcing will remain difficult for the 2025/26 season.

Prices move sideways due to conflicting data: producers forecast low yields while EU/IOC maintain higher estimates.

Geopolitical tensions in the Strait of Hormuz pushed crude oil toward $120/bbl, triggering an Emergency Fuel Surcharge on March 25, 2026. Higher energy costs increase bottling overhead and plastic packaging prices. Additionally, the World Bank Fertilizer Price Index rose 6.5% this month, signaling higher agricultural input costs for Q3.

These factors establish a higher cost floor for landed goods. We recommend partners include these surcharges in 2026 budgets.

Our team is at Alimentaria Barcelona (March 23–26). Please contact us to schedule a meeting regarding volume planning and sustainability.

Olive Oil Times,

Poolred,

Ismea Mercati,

Junta de Andalucia,

Teatro Naturale,

International Olive Oil Council

Share on