Prices start to ease in nearly all Mediterranean countries after autumn rain.

What’s happening this month?

The autumn rain in nearly all Mediterranean countries, along with the start of the new harvest and positive expectations for overall yield, has contributed to a decline in prices over the past few weeks, especially after Turkey recently lifted its export ban.

The month of October was marked by severe flash-storms in parts of Spain, leading to three days of national mourning due to the unprecedented number of deaths caused by flooding and buildings collapsing in densely populated areas.

The olive plantations in Andalusia, Spain’s largest olive oil-producing region, experienced no significant damage, aside from a delay in harvesting activities.

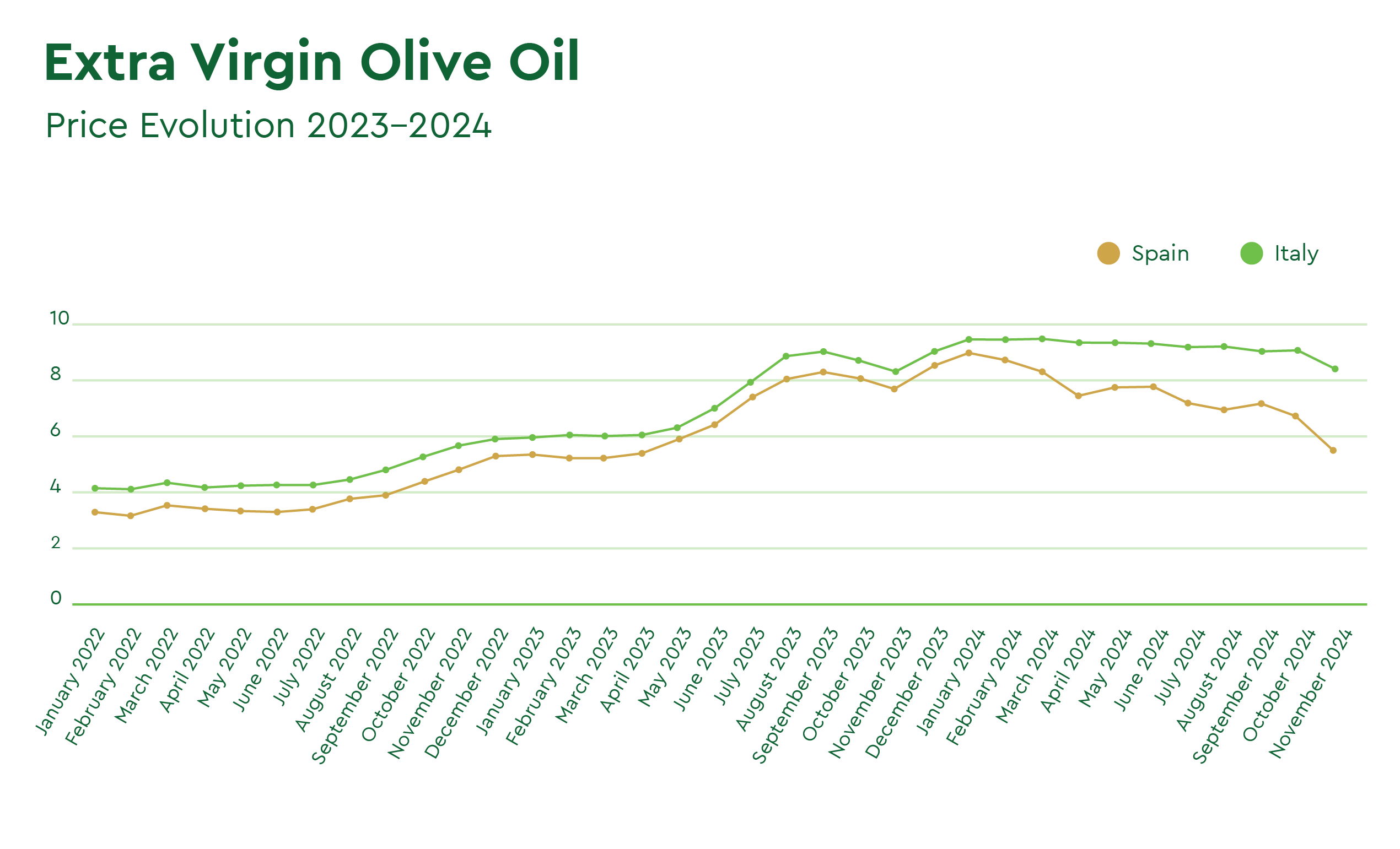

In Spain, the global market leader in olive oil production, prices have decreased by over 1.50 Eu/Kg in just four weeks and could keep declining further in the coming months. Similarly, Italy is also experiencing a gradual easing of prices, declining from the peak level of 9.50 Eu/Kg, despite the shallow carryover volumes from last year and the negative volume projections for the ongoing crop.

As of November 22nd, Poolred and ISMEA, two reliable platforms monitoring fluctuations in average trade values in Spain and Italy, reported the following prices:

Spain: 5.55 Eu/Kg (Poolred)** → approx. -23% versus the previous month

Italy: 8.50 Eu/Kg (Ismea)** → approx. -7% versus the previous month

Greece: 5.87 Eu/Kg (Ismea)** → approx. -18% versus the previous month

Tunisia: 5.43 Eu/Kg (Ismea)** → approx. -22% versus the previous month

**Trade platforms often overlook variations in quality and grade. Our sourcing team suggests anticipating a premium of at least 0.20 to 0.30 Eu/Kg for certified, traceable batches, as well as for high-quality extra virgin olive oil that is suitable for export and has low pesticide residues.

After two years of exceptionally high retail prices, the olive oil sector is now facing pressure from clients to lower prices back to pre-crisis levels. This demand comes as home consumption declines and competition from seed oils increases. Meanwhile, farmers and smaller producers in countries experiencing rising labor and energy costs hope to maintain at least some of the premium pricing achieved in the recent months.

In this context, larger companies with in-house inventory and greater financial resources may decide to wait before entering the market, anticipating further price declines. In contrast, smaller companies or those without leftover stock from the previous year may need to restock their inventory sooner. This situation could create demand and potentially lead to new price spikes.

Sources: Poolred, Ismeamercati

Spain’s balance sheet of October

Since the harvest began, Spanish producers have introduced only 36,000 Tons of new olive oil into the national reserves. This figure is slightly below the production amount for October 2023, which was 38,370 Tons. Despite the optimistic expectations on new total volumes available for this season, autumn rains delayed harvesting activities, and many oil mills are not yet fully operational.

The demand for olive oil remains strong in October, marking the beginning of the 2024-25 harvest cycle. The Spanish Ministry of Agriculture, Fisheries, and Food has reported a release of 104,000 Tons of olive oil onto the market. This figure is almost 30% higher than the market releases from the previous year.

The carryover from the 2023/24 harvest remains significantly low, at just 186,000 Tons compared to 248,000 Tons from last year, as detailed in the balance sheet for October 2024 (in 1000 Tons, rounded):

186 Tons (carry over 2023/24)

+ 36 Tons (production OCT)

+ 20 Tons (approx imports)

– 104 Tons (releases to the market)

————————————————————

138 Tons (Stock Situation Spain by October 2024)

The Spanish olive oil sector is starting the new crop cycle with reserves that are 37% lower than in October 2023. However, it is expected that stocks will quickly rebuild in the coming months as olives are harvested and brought to the mills, leading to an increase in the availability of fresh and extra virgin olive oil.

Harvest prospects in Greece and Turkey 2024/25

The consistently high temperatures and ongoing lack of rainfall have resulted in reduced yields for olive oil production in Greece. Key growing regions, particularly on the Peloponnese peninsula, as well as islands such as Crete and Lesbos, have reported significant crop losses.

Several Greek farmers are postponing their harvest operations until mid-November, hoping that rain and cooler temperatures will slightly boost olive oil yields. This situation primarily impacts areas where irrigation is limited or not possible due to geographical conditions, making them dependent solely on rainfall for irrigation.

Despite all, Greece currently anticipates a total harvest of 250,000 – 270,000 Tons and to make a significant contribution to global production this crop year, exceeding Italy’s total production and competing with emerging players such as Turkey, Tunisia, and Morocco.

An article in Olive Oil Times reports that Turkey may achieve a local harvest yield of 475,000 Tons. If these figures are verified, Turkey would surpass its previous record harvest of 421,000 Tons from the 2022/23 season and would rank second, following market leader Spain, leading at over 1,400,000 Tons between Olive Oil and Extra Virgin Olive Oil.

Positive expectations for this year’s harvest, along with renewed efforts by Turkish producers to enter the global market, are likely to attract the attention of international retailers. However, there remains uncertainty regarding supply stability. The Turkish government has recently lifted its export ban on bulk olive oil, but it may choose to regulate exports again in the future. If internal political decisions allow for unrestricted exports, Turkey is expected to significantly increase its olive oil availability this year, which is already beginning to impact global prices.

Final thoughts

The current climatic and political conditions in Turkey indicate a significantly high availability of olive oil and experts generally agree that global production could exceed 3 million Tons this year.

There was little doubt that prices would begin to decrease with the arrival of the new harvest. However, many experts, traders, and analysts did not anticipate the drop being sudden or significant, especially given the delays in operations in Spain and the low inventory left from the previous harvest.

Considering the current circumstances, it would not be surprising to see the price of Spanish conventional olive oil range from 4 to 5 Eu/Kg by the first quarter of 2025. This would bring back the market to the evaluations experienced two years ago, before climate-related and geopolitical factors led to a sharp and unprecedented increase.

The focus now could shift to understand and anticipate further potential decline in average prices in Spain and how Tunisia, Morocco, and Turkey will approach international trade valuation. Additionally, it will be important to see how Italy, Portugal and Greece—known for their reputation and commitment to organic, certified and high-quality Extra Virgin Olive Oils—will defend their market position in the face of increasing competition and retail pressure.

Italian regions like Tuscany, Puglia and Sicily are well-known and highly valued for their exceptional Extra virgin olive oils. This year, the relatively lower availability suggests that prices for Italian Evoo, although they may go lower, are likely to remain relatively stable across 2025.

Our sourcing experts predict that the market will have a clearer understanding of the quality and volumes available by the end of November. Farmers may also provide a forecast for 2026 in the spring of 2025, allowing players to develop a medium-term vision and strategy.

As we approach these milestones, we recommend covering demand by maintaining a short position while closely monitoring the market and being prepared to move quickly and decisively as soon as the market stabilizes.

Please don’t hesitate to reach out if you have any questions and would like to work with us on expanding your private label portfolio or are interested in a free consultation.

Share on