Price Adjustments Continue, Demand Grows Steadily

5 MIN READ

By Franziska Finck — June 26, 2025

Our Monthly Olive Oil Market Report blends real-time data with field insights to support your private label retail strategy.

Want it monthly?

Sign up here|

Getting your Trinity Audio player ready...

|

What’s happening this month?

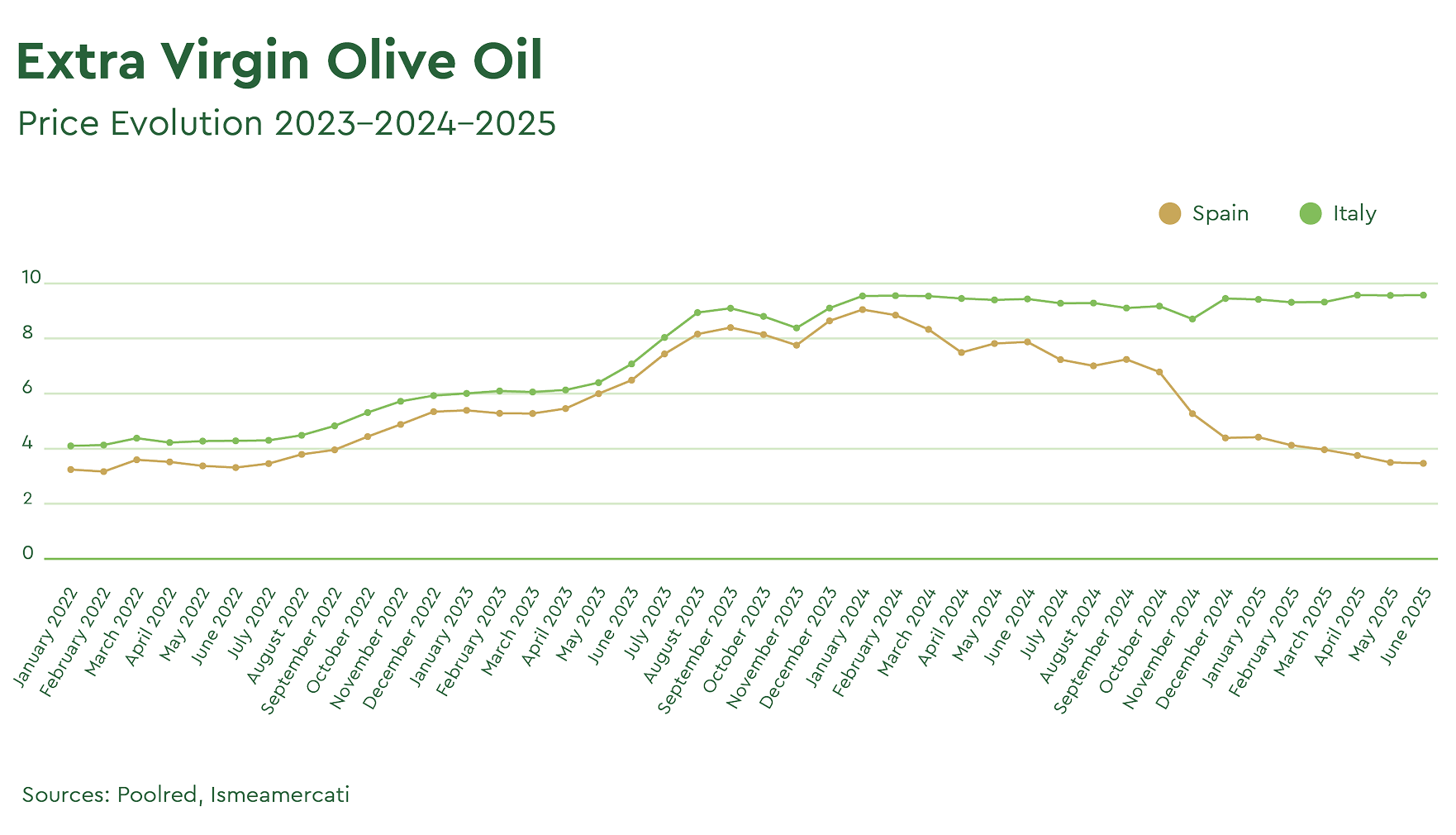

After a brief period of price stabilization, olive oil prices have again edged downward in recent days, though the declines remain marginal.

A review of key market platforms monitoring average evaluations, while often not reflective of actual transaction prices for high-quality olive oils, provides a snapshot of current national trends:

*Starting this month, price data from Junta de Andalucía and ISMEA will be included alongside Poolred to offer a more comprehensive view of the Spanish market. Although all three primarily track base olive oils, the triangulation helps clarify broader trends.

In Spain, by far the world’s largest producer, prices are now back at levels seen during the 2021/22 campaign. Prices have settled near break-even levels, offering little margin for producers and deepening dissatisfaction throughout the farming sector.

As the market leader, Spain is also influencing other Mediterranean countries, which are following suit with further price reductions to avoid losing market share.

Italy remains an outlier. The consequences of a low-yield harvest are keeping domestic olive oil prices at a significant premium over those of other producing countries. This price gap may prompt international buyers to explore alternative sourcing options more frequently.

Spain’s Balance Sheet – Demand Holds Firm

In May, Spain recorded olive oil sales of 120,095 Tons (excluding imports). According to Olimerca, this figure, endorsed by Spain’s Ministry of Agriculture and the AICA, is seen as “an excellent result.” It marks a 21% increase over the eight-month average of 99,000 Tons, illustrating how recent price corrections have stimulated market activity.

Jesús Cózar Pérez, Secretary General of UPA-Andalusia, noted:

“in the eight months of the current marketing campaign, from October 2024 to May 2025, olive oil sales have already reached one million Tons – representing over 70% of total production. If this trend continues, by the end of the campaign, we will have sold more olive oil than we produced.”

As of May 2025, Spain’s accumulated olive oil production for the 2024/2025 season has reached 1,414,124 Tons, and to date, approximately 840,000 Tons (without imports) have been released to the market.

If the current sales pace continues through the summer months, the carryover could be estimated at around 300,000 Tons by October.

The market awaits official production data, but early signs across key regions suggest an optimistic outlook for the next olive oil campaign.

EU Olive Oil Production Rebounds in 2024/25

According to an article in the online Spanish magazine Mercacei, olive oil production across the European Union has reached approximately 2.1 million Tons as of April 2025, marking a strong recovery compared to the previous season.

Spain leads the global olive oil market with 1.41 million Tons, around 40% of worldwide production, grown on 2.8 million hectares. Greece (250,000 Tons), Italy (247,000 Tons), and Portugal (177,000 Tons) follow.

Total EU olive oil output for 2024/25 is estimated to be at around 2.1 million Tons, an increase of nearly 40% compared to the 1.53 million Tons produced last season. Spain, Greece, and Portugal have contributed to the rebound, while Italy’s production declined by 25% due to climate-related challenges.

EU olive oil consumption is expected to remain stable at 1.24 million Tons, while final stock levels are projected to increase slightly to 352,000 Tons, indicating improved availability across the region.

In a recent article by Olive Oil Times, Spain’s Minister of Agriculture suggested that global olive oil production could even reach 4 million Tons, driven by efforts to double current output and reinforce Spain’s leadership in the international market.

However, industry analysts have questioned the feasibility of this target, viewing it as overly ambitious given current structural and climatic constraints.

Final thoughts

The global olive oil market remains balanced between robust demand and significant operational challenges.

A key concern is the pending review of U.S. tariffs on EU olive oil, currently set at 10% but scheduled for potential revision after July 9.

Without a renewed trade deal, import taxes may exceed 50%, placing substantial pressure on U.S. buyers, retailers, and suppliers. The U.S. domestic production, concentrated in California, currently accounts for less than 4% of the nation’s olive oil demand for this healthy ingredient.

In preparation for the event, many olive oil producers are currently fast-tracking shipments to the United States to minimise exposure to potential increases in duties. In parallel, industry discussions are intensifying around the possibility of relocating bottling operations to the U.S. as a strategic measure to reduce the long-term impact of future trade restrictions and protect market accessibility.

Meanwhile, the Spanish domestic market is seeing a significant decline in consumer prices following last year’s record highs. Some local producers have expressed concern that the combination of falling price levels, aggressive discounting by supermarkets, and intensifying global competition could place further pressure on already narrow margins, threatening the sector’s overall profitability.

In recent weeks, the olive oil trade and bulk market have seen a marked increase in demand and transactions. This resurgence is being driven by a combination of more attractive pricing across key origins and a surge in export activity tied to evolving U.S. policy decisions.

For deeper market insights or tailored support in launching or expanding your private label olive oil programs, please reach out to our international team of experts.

Share on