Prices at the origin continue to decline, with one exception.

5 MIN READ

By Franziska Finck — January 22, 2025

Our Monthly Olive Oil Market Report blends real-time data with field insights to support your private label retail strategy.

Want it monthly?

Sign up here|

Getting your Trinity Audio player ready...

|

What’s happening this month?

Since December 2024, the olive oil market has continued to experience price declines across most Mediterranean countries, with Italy as a notable exception.

According to ISMEA, the leading Italian commodity trade monitor platform, the evaluation of the Italian Extra Virgin Olive Oil in 2025 remains substantially in line with 2024, fundamentally immune to the forces responsible for halving the price of Olive Oil and Extra Virgin Olive Oil produced in other regions.

Here is a snapshot from mid-January, with prices from three major producing countries in the Mediterranean during the second week of January:

– Spain: 4.50 Eu/Kg

– Greece: 5.60 Eu/Kg

– Tunisia: 4.00 Eu/Kg

And the past three months’ trend for Italian Extra Virgin Olive Oil:

– November 24: 8.73 Eu/Kg

– December 24: 9.45 Eu/Kg

– January 25: 9.50 Eu/Kg

The combination of heat and water scarcity in its southern regions, the effects of Xyella, and the natural cycle of rest for the Olive tree could slide Italy from being the second largest producer in the world to the fifth or even sixth position, surpassed by Spain, Greece, Portugal, Tunisia, Morocco, and Turkey.

After two years of narrowing price gaps in the higher end of the market, we may see a return to historical trends. Italian Extra Virgin Olive Oil is poised to lead the market once again with the highest valuations, while Spain may widen the gap, reclaiming its status as the key volume player and value trendsetter for most of the other producing countries.

Spain’s balance sheet of December

Spain’s position as a leading olive oil consumer and producer has been challenged during the last two years of reduced production and falling internal consumption. The local government and producers have taken the situation seriously, reducing the taxation on olive oil to make it more accessible to its citizens and investing in research, technology, promotion, and production.

With clear signs of recovery ahead, the Spanish government has recently released its current balance sheet for olive oil consisting of last year’s reserves and new production.

The current reserves amount to 823,729 Tons, divided as follows:

– Cooperatives – 683,854 Tons

– Packers – 135,561 Tons

– PCO (public storage) – 4,315 Tons

These figures tell us that 77% of the olive oil is still in the oil mills hands and only 15% is with bottlers and traders. At the end of 2024, the country’s total production landed at 883,589 Tons, with December’s production alone weighing 584,499 Tons.

Assuming Spain will produce an additional 300,000 to 400,000 Tons in January and around 150,000 Tons in February, it is safe to assume that the final total forecast for the 2024/25 harvest could be at least 1,300,000 Tons, in line with the pre-crisis level.

Despite positive volume projections and falling prices, Spanish oil consumption and exports have not increased significantly. So far, only 87,249 Tons have been reported as sold, showing that producers and major players might be waiting for more clarity on global dynamics and demand.

International Olive Council: Global Forecast and Trends

The International Olive Council (IOC) is the largest and leading intergovernmental organization entirely focused on olive oil and table olives. They regularly publish updated guidelines on farming practices, quality standards, testing protocols, and data related to production forecasts and trends.

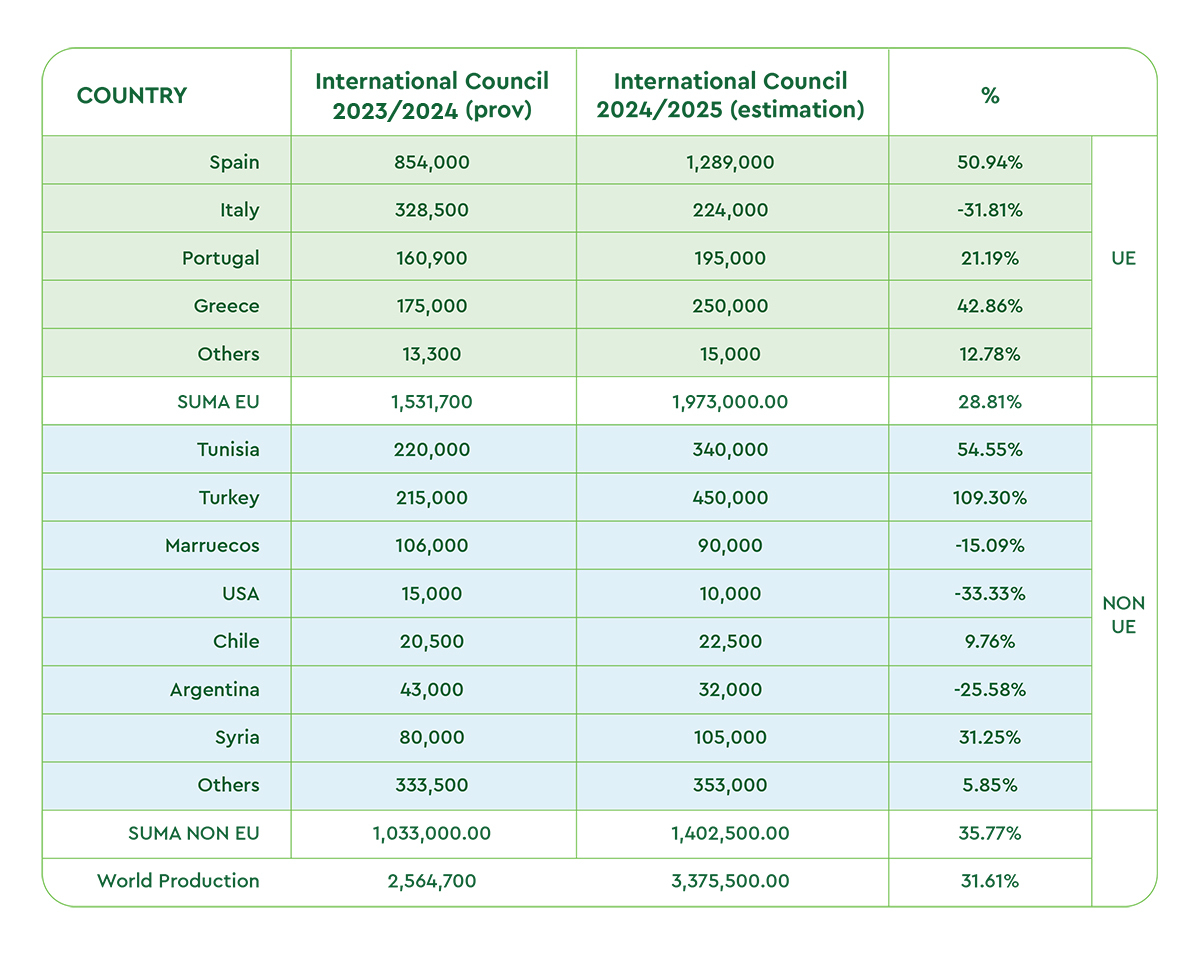

According to the IOC and an article from the Olive Oil Times analyzing their data, we could expect a total production of 3,375,500 Tons of olive oil for the 2024/25 harvest year across all grades. If these estimates are accurate, this would represent an increase of approximately 32% compared to the 2023/24 harvest.

Specifically, production in EU countries is set to rise by 29%, while non-EU countries could see an increase of 36%, as illustrated in the chart below.

As the figures show, all EU countries except Italy are showing growth compared to the previous year. Countries such as Tunisia and Turkey project record harvests in 2024/25 and are making a decisive contribution to global production.

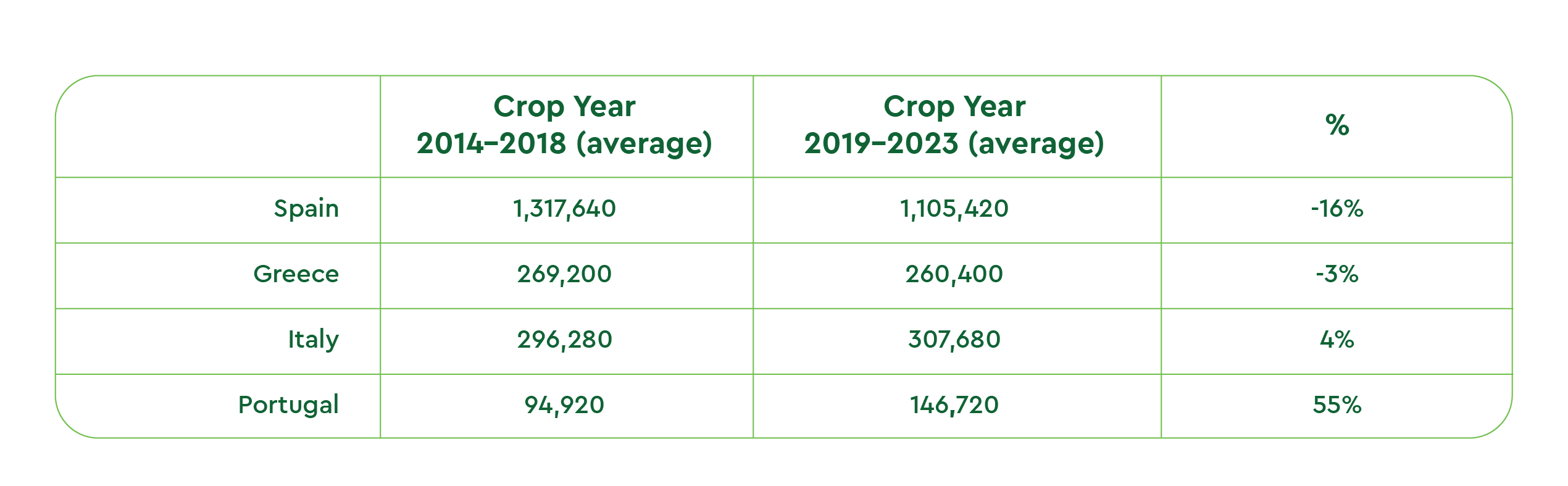

If we compare the average crop year results from 2024 – 2018 versus crop 2019 – 2023, we can also see that olive oil production worldwide has moved up by just 1% in the last 5 years, and in Europe it has even fallen by – 8%:

When examining the individual EU countries, here is the breakdown:

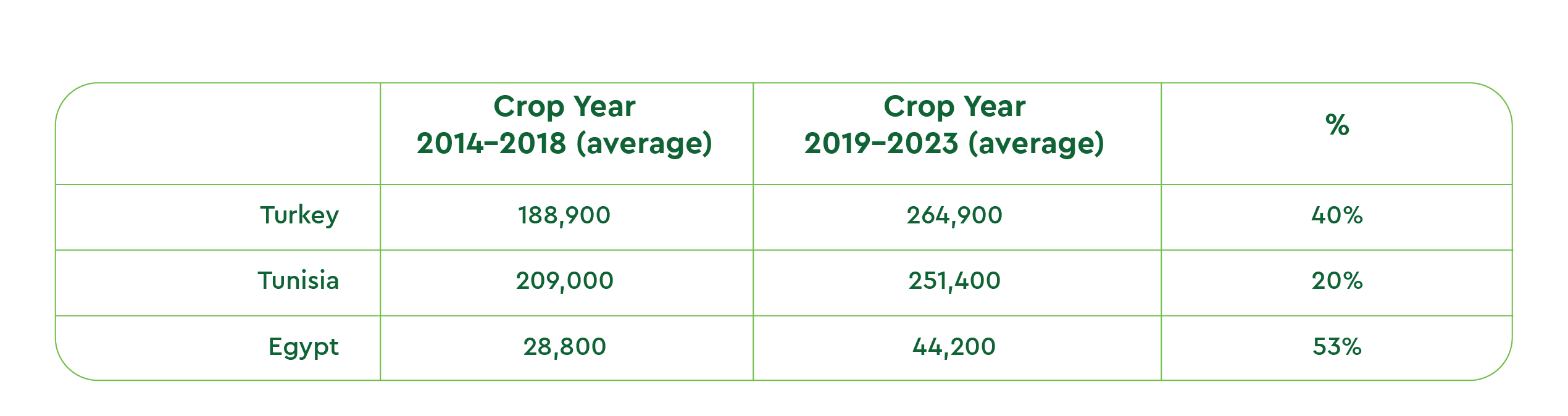

A few non-EU countries have been compensating for the production decline in other nations:

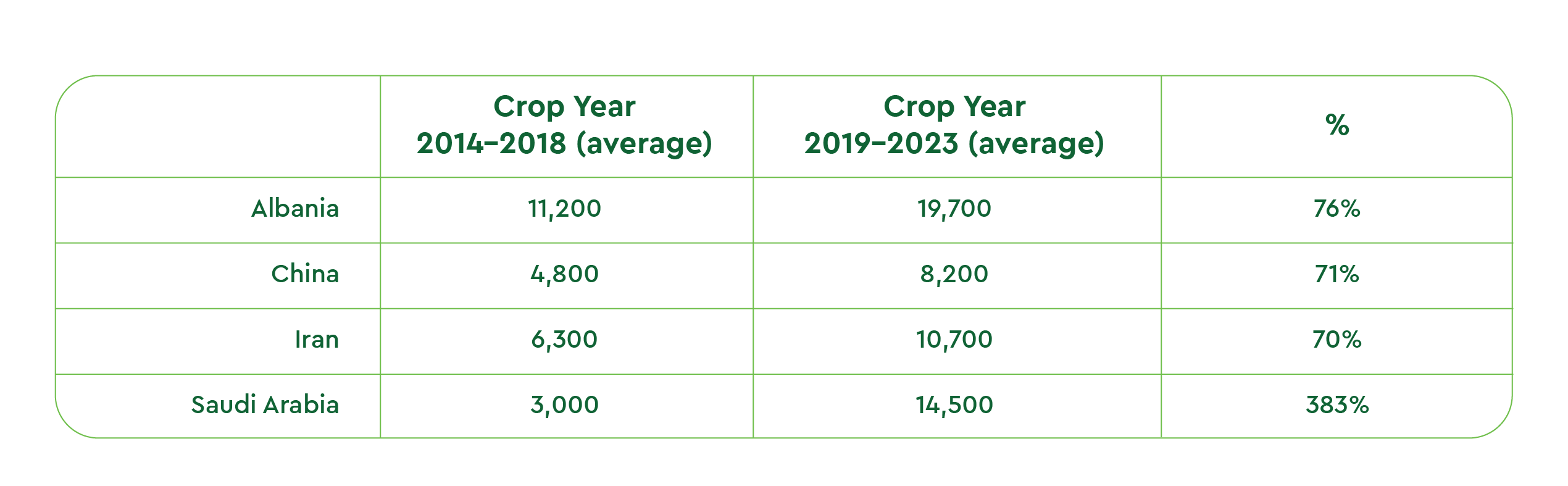

Worth also mentioning the countries with the greatest percentage increase in recent years:

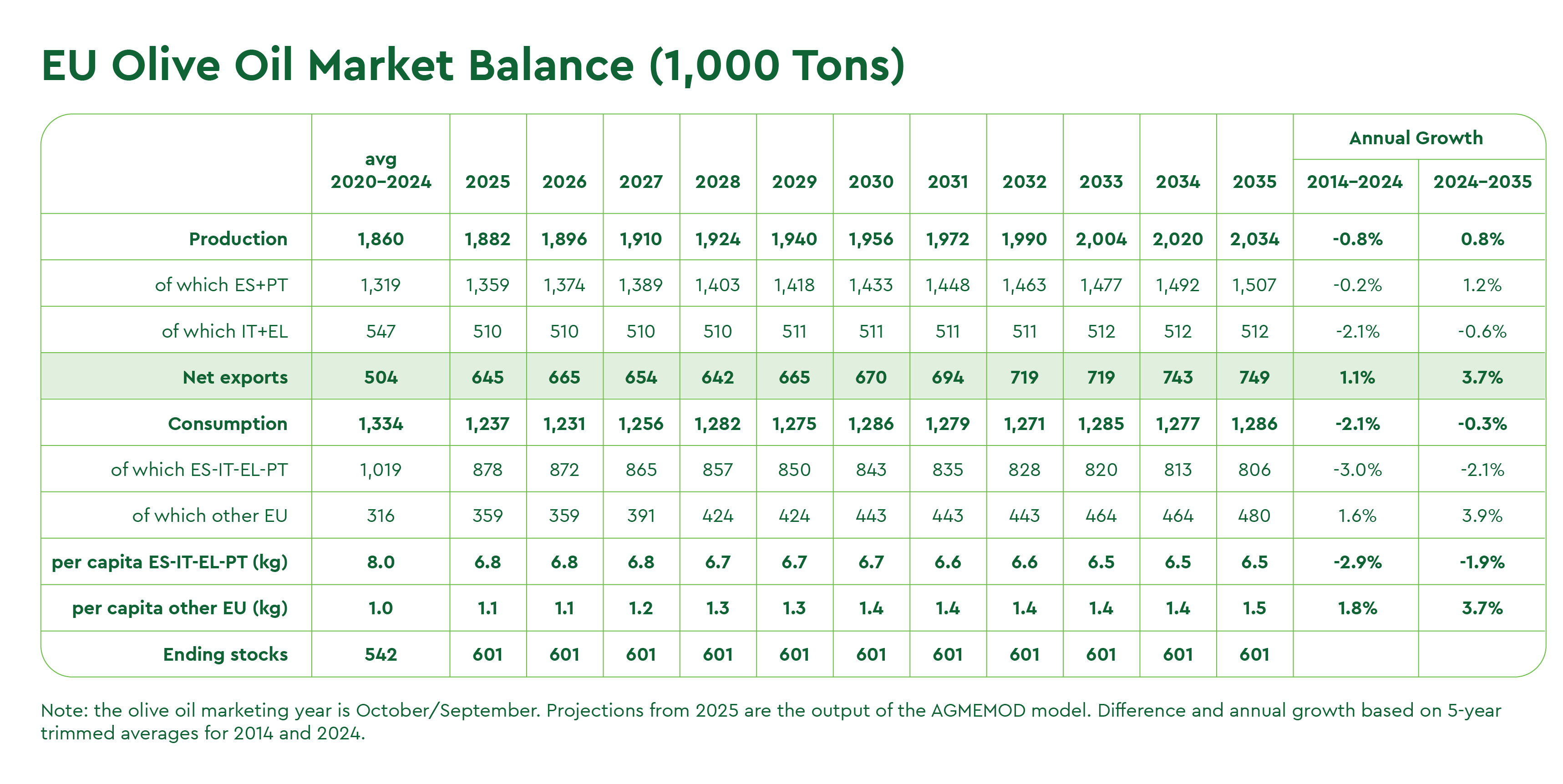

European Commission Outlook: Climate and Consumption

The annual report “EU Agricultural Outlook“, in which the European Commission presents its forecasts of agricultural developments over the next 10 years, also touches on olive oil production and consumption trends.

The EU foresees a slight increase of 1.2% in Spain and 1% in Portugal’s olive farming output for the next decade, thanks to new super-intensive plantations. In Greece and Italy, on the other hand, we could see a decline in the hectares dedicated to olive farming, which could lead to further decreases in production during the same period.

Farming experts believe that the future of olive oil in Europe will depend significantly on how each country adapts and manages climatic changes, including water shortages and temperature anomalies.

The EU Commission reports also on local olive oil consumption. In 2010, 1.79 million liters were consumed, while between 2020 and 2024, the average consumption in the EU was 1.33 million liters.

The forecasts for the next few years indicate a relatively stable trend, with an expected usage of around 1.2 million (a decrease of 0.3%) in the EU zone. This projection reflects a balance between declining consumption in Spain, Greece, and Italy and new opportunities in regions where this condiment has not yet become a pantry staple.

USA-EU trade value and tariffs

According to the trade magazine Food Navigator and the European Commission data, American businesses have spent an additional €1.5 billion on European food imports year-on-year between January and July 2024.

In the first half of 2024, the value of EU olive and olive oil sales alone increased by nearly two-thirds, totaling €1.7 billion compared to 2023, driven by value.

This information, combined with President Trump’s campaign proposal to implement a tariff on all foreign-imported products once in office and the fact that the whole US olive oil production covers less than 5% of national growing consumption, raises uncertainties for all olive oil businesses and enthusiasts in the USA and Europe, as we enter the new year.

A new tax, like the 25% imposed in the past on Spanish bottled olive oil, could significantly increase the cost for US businesses importing olive oil from the EU, from specific regions, or as a whole.

Final thoughts

In the past two years, retailers and wholesalers have been positively surprised by the relatively small drop in volume sales, considering the sharp price increase at the source and on the shelf, showing a solid and growing appreciation for Extra Virgin Olive Oil and Olive Oil from families worldwide.

We are now observing prices declining again, while demand and trade operations are not increasing at the same rate.

Many businesses and trade players might be wondering if olive oil prices at the source have finally reached the lowest level and if they should wait a little longer as they feel the pressure to close contracts securing volumes and quality batches for the year.

As the market self-regulates and without considering the looming tariffs that could affect the food industry, we think that Spanish producers and traders will soon signal the market in one way or another.

We recommend that all our business partners and friends maintain strong connections with the source and closely monitor Spain’s harvest and rainfall forecasts. Be prepared to make quick decisions and take action based on the advice of trusted local advisors.

Share on