Olive Oil Prices continue to drop in Spain amid rising production and favorable weather.

5 MIN READ

By Franziska Finck — March 25, 2025

Our Monthly Olive Oil Market Report blends real-time data with field insights to support your private label retail strategy.

Want it monthly?

Sign up here|

Getting your Trinity Audio player ready...

|

What’s happening this month?

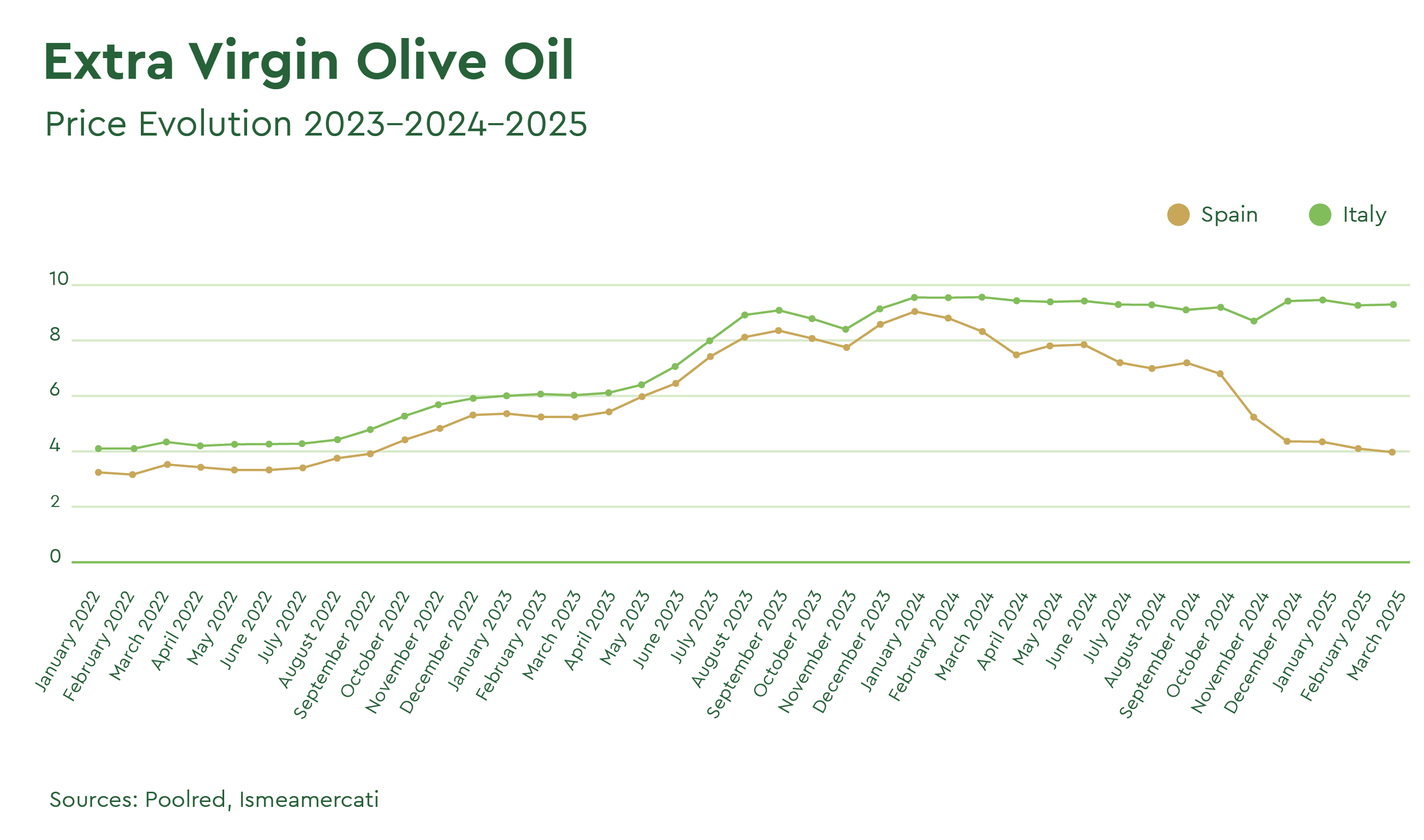

Over the past few weeks, average extra virgin olive oil prices (EVOO) prices in Spain have continued a downward trajectory, once again dipping below the 4.00 Eu/Kg threshold, at approximately 3.8 to 5 Eu/Kg for conventional and 5 to 5.5 Eu/Kg for organic. This correction is primarily attributed to a substantial increase in production volumes compared to the past two years, now forecasted to reach 1.45 million Tons, for all olive oil grades combined.

Abundant rainfall across key producing Spanish regions over the last 15 days has also contributed to improving the current crop conditions and reinforced positive expectations for future harvests as well.

Demand and offer for Spanish olive oils remain solid, as demonstrated by the strong market activity in February, except for premium-quality EVOO with low pesticide residuals and matching most international export standards, for which the availability remains limited. As a consequence, there are fewer transactions. This situation has, in turn, helped to slow down the pace of price reductions for the other grades as well.

Italian EVOO, with lower than average volume production, has remained elevated, with trading at approximately 9.55 Eu/Kg for conventional and 10.40 Eu/Kg for organic grades.

The Tunisian market continues to experience upward pressure, with conventional EVOO evaluations close to the Spanish origin, averaging at 4.00 Eu/Kg and organic at 4.30 Eu/Kg. Greece and Portugal remain stable, showing no significant price deviations from last month.

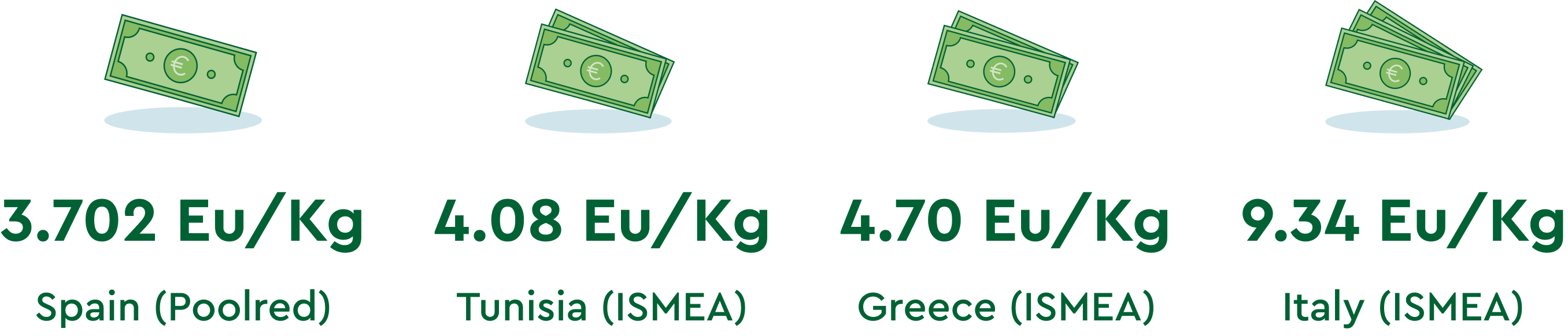

On March 21st, average price levels from Poolred (Spain) and ISMEA (Italy, Tunisia, and Greece) show:

Note: All prices provided are estimates based on market research and can vary.

This month, key topics across international trade media have focused on evolving trade dynamics, shifting consumption patterns, and recent regulatory developments. Below is a summary of the most relevant updates impacting the global olive oil industry:

Olive Oil Trade: Spain, Italy, Tunisia, and Turkey Dominate U.S. Market

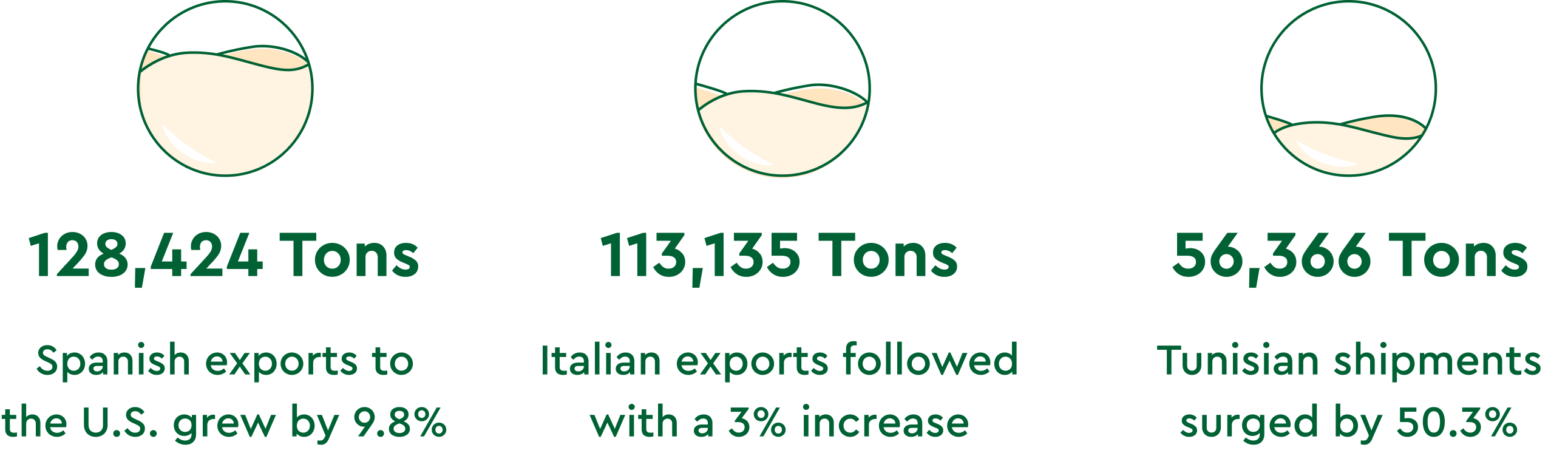

According to the most recent trade data, U.S. olive oil imports reached 362,618 Tons in the 2023/24 season, marking a modest 1% year-over-year increase. Spain, Italy, Tunisia, and Turkey collectively accounted for 86% of total U.S. imports, consolidating their position as key global suppliers.

The European Union remains the dominant trade partner of the United States, averaging 252,000 Tons per season, valued at €1.228 billion. In the current campaign, export values to the U.S. escalated by 64.6%, reaching €2.077 billion, driven primarily by price inflation rather than volume growth.

The unit export value from the EU to the U.S. peaked in July 2024 at €987.8/100 Kg, compared to €517.9/100 Kg in December 2022 and €298.8/100 Kg in September 2020. These figures underscore the results of two consecutive crop failures in Spain, growing cost pressures faced by importers, the shifting dynamics of global trade and household penetration.

It is important to highlight that the United States produces less than 5% of the extra virgin olive oil required to meet domestic consumption needs. As such, any potential reintroduction of tariffs on EU olive oil—currently under discussion—could significantly undermine the competitiveness of Mediterranean producers in the U.S. market and lead to increased procurement costs for North American retailers and distributors.

EU Removes Tariffs on Chilean Olive Oil

The European Union has officially removed import tariffs on Chilean olive oil, under a new trade agreement designed to enhance bilateral economic relations. The removal of tariffs—previously up to 10%—is expected to boost Chilean market penetration in Europe, intensifying competition with traditional Mediterranean suppliers, historically responsible for approx 80% of the global supply.

Chile, already recognized for its high-quality extra virgin olive oils, stands to benefit from improved price positioning and expanded access to European buyers. While this development presents new opportunities for Chilean exporters, it may also pose challenges for EU producers already contending with production volatility and rising input costs.

The long-term impact will depend on how quickly Chilean exports scale up and how traditional producers adapt to this evolving competitive landscape.

Global Olive Oil Consumption Set to Rise by 10% in 2024/25, while EU Consumption Declines

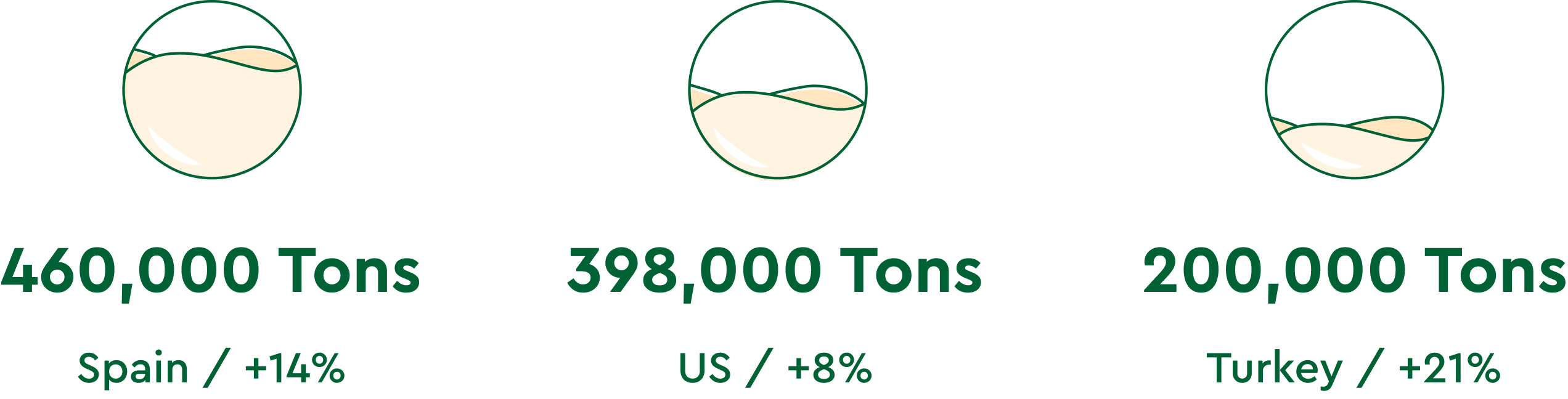

For the International Olive Council (IOC), the global olive oil consumption is expected to grow by 10% in the 2024/25 season, reaching 3,064,500 Tons. This projection follows the decline experienced in 2023/24, where consumption dipped 2.6% YoY to 2,780,000 Tons, as a direct consequence of high prices.

Specifically, EU consumption is expected to reach 1,326,000 Tons (+7%), with Spain accounting for 460,000 Tons (+14%), followed by the United States with 398,000 Tons (+8%), and Turkey with 200,000 Tons (+21%).

Interestingly, the International Olive Council (IOC) highlights a sustained downward trend in olive oil consumption within the European Union (EU). While total global consumption has nearly doubled since the 1990/91 season, the EU’s share has declined markedly—from over 70% in 2004/05 to approximately 45% in recent years. This reduction has been largely offset by growing consumption in non-IOC member countries and other emerging IOC markets, underscoring a geographic shift in global demand dynamics.

Final Thoughts

Recent market developments point to a notable shift in global olive oil dynamics compared to 2024.

However, high-quality extra virgin olive oil from the largest producer in the world remains scarce, and the pace of price reductions may slow in the coming weeks. At the same time, international trade trends reveal shifting consumption patterns, with a gradual decline in EU consumption being offset by rising demand in non-EU markets.

The United States—where domestic production accounts for less than 5% of consumption—remains a critical trade partner for Mediterranean exporters, responsible for approx. 80% of the global supply. The looming risk of U.S. imposed tariff on olive oil could significantly impact EU export competitiveness and raise costs for North American buyers.

In light of these factors, securing inventory in the short term could prove strategically advantageous for businesses active in the U.S. market. In parallel, remaining open to alternative sourcing origins and investing in supply chain flexibility may represent a long-term competitive advantage for all global operators.

For further insights or inquiries, please don’t hesitate to reach out to our international team.

We’re here to support your strategic decisions and provide tailored solutions.

Share on